SUBJECT TO CHANGE.

“One must change one’s tactics every ten years

if one wishes to maintain one’s superiority.”

Napoleon Bonaparte

Three things have been true since I started my investing career.

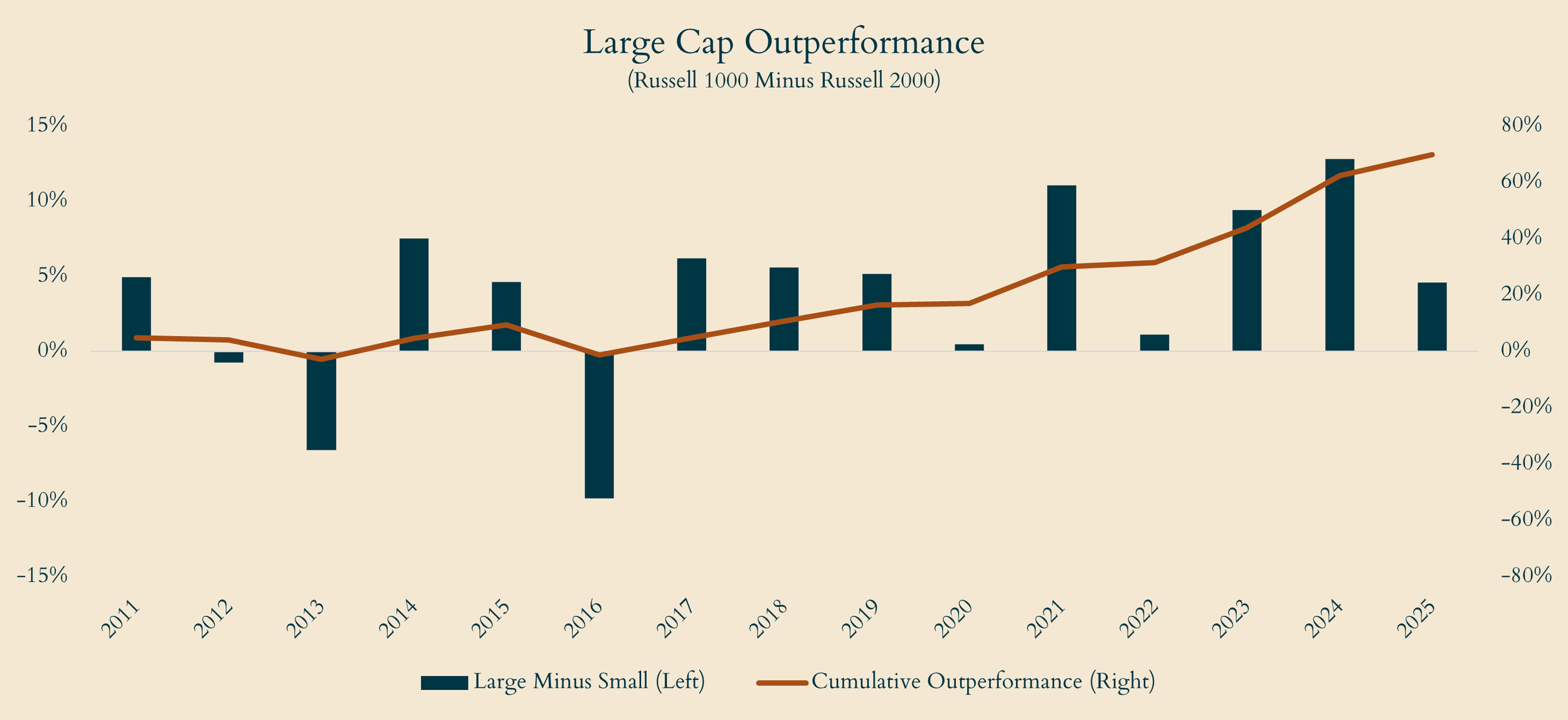

· Large caps outperformed small.

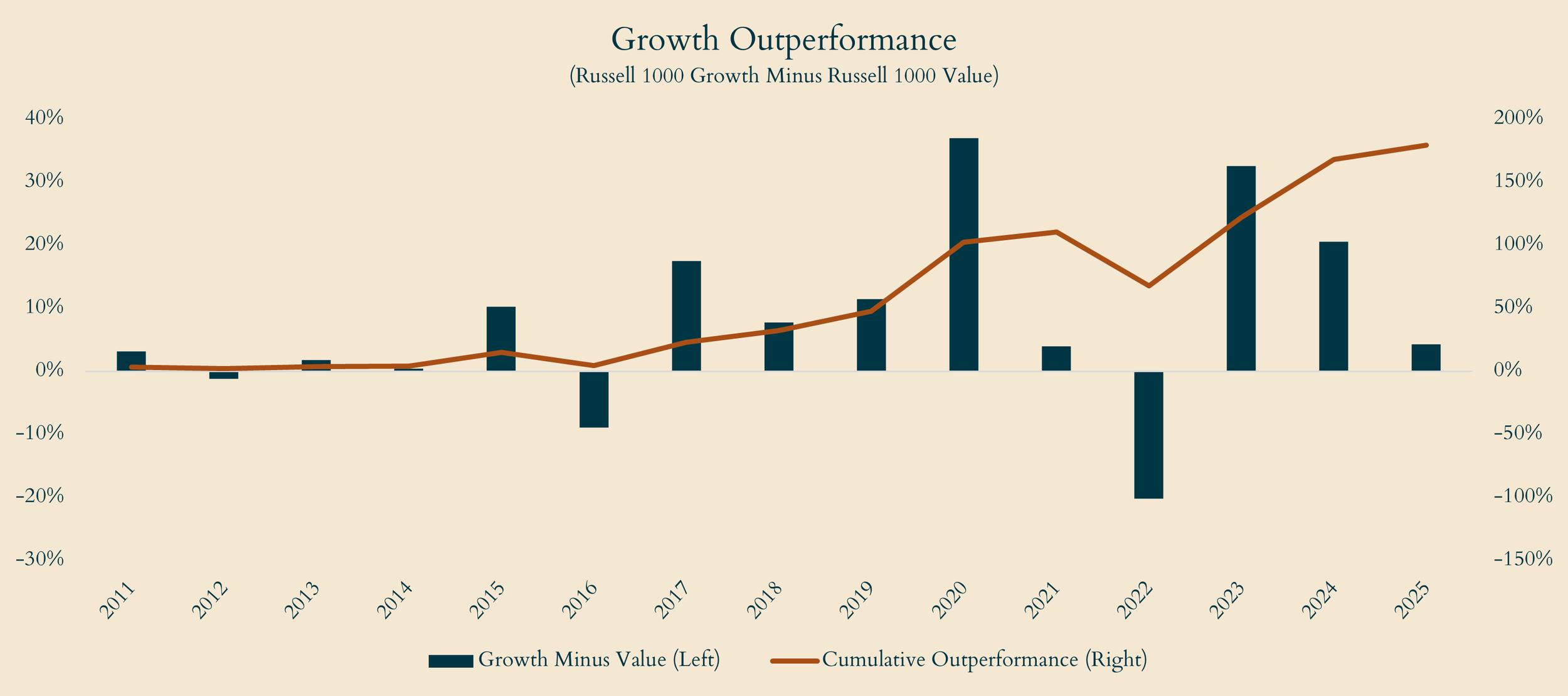

· Growth outperformed value.

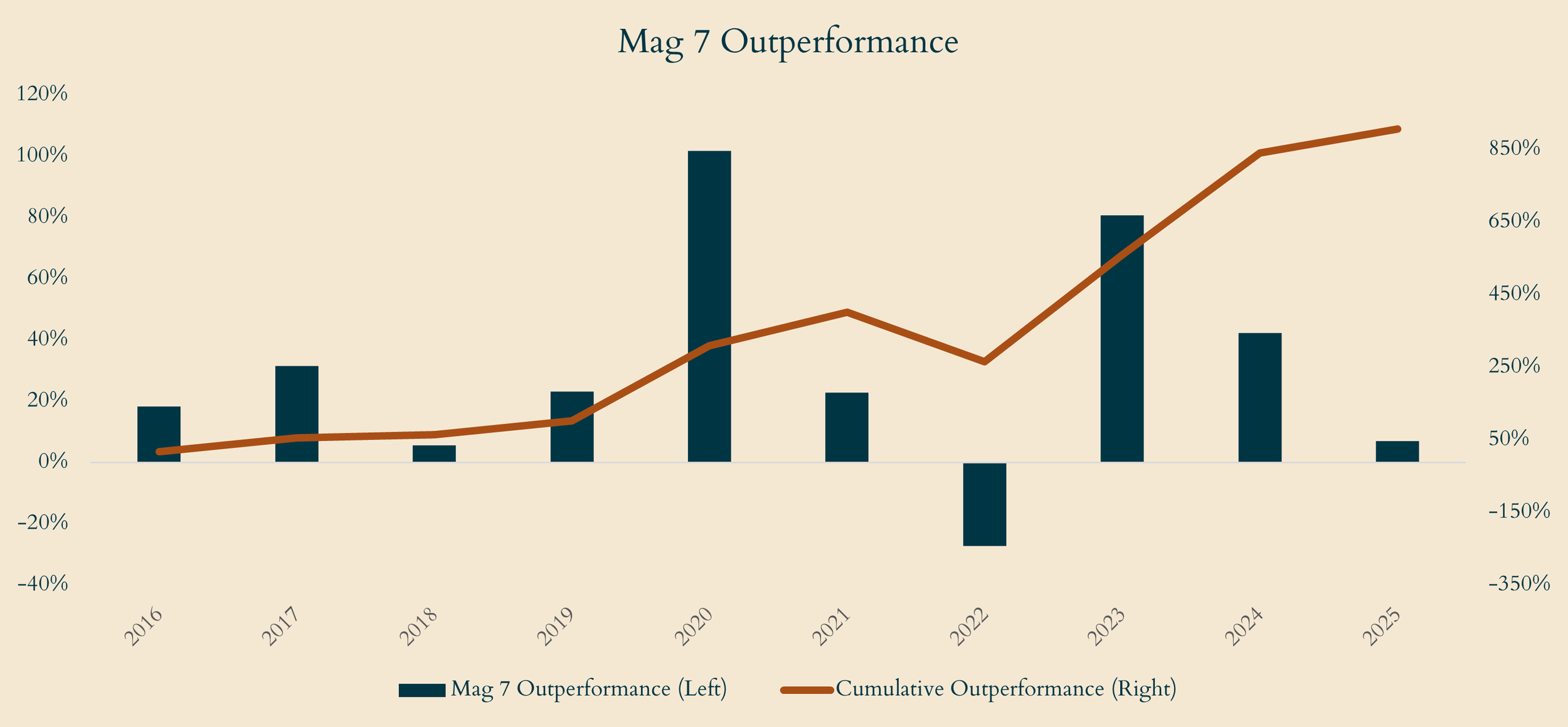

· The Magnificent Seven outperformed everything.

Contrarians have said for years that these trends couldn’t, wouldn’t or shouldn’t persist. They reminded us that trees don’t grow to the sky or if something can’t go on forever, it will stop. Well-armed with arcane academic studies or historical comparisons to the distant past, they explained how markets are supposed to be, while conveniently ignoring how they are. Their observations were mildly interesting (if you like that sort of thing), but have consistently been early, which is a diplomatic way of saying wrong.

But even a lopsided coin comes up heads eventually and I suspect the tide is turning in their favor (full disclosure: I’m half-contrarian myself, on my mother’s side). One of the reasons I like investing is that markets constantly change or at least they used to. When healthy, they’re naturally self-correcting, because if investors get too excited about a company’s prospects, they bid it up, lowering returns in the process. Like the childhood game King of the Mountain, the ten largest companies change every few years because no one stays on top forever. The defining characteristic of a market is flux, yet for most of my career they’ve been remarkably fluxless. Let me elaborate.

I began my career in small cap investing, not realizing that large caps would outperform small caps 12 of the next 15 years. I suppose there’s good reason for this. The number of public companies is half of what it was in 1996. A unicorn is a private business worth at least $1 billion or more, and like most mythical creatures, are meant to be rare. Thanks to the rise of private equity, we now have 850 such one-horned wonders. As companies stay private longer, the quality of the average small cap has deteriorated. Since the best stocks are eventually asked to leave when they get too big, the index relies upon new blood to revitalize the gene pool. Many of the recent additions have been of dubious quality, either pre-revenue biotechs or unprofitable SPACs, which has left the average small cap below average.

I also cut my teeth in value investing, which was once popular, but has recently fallen on hard times. Little did I know that value would underperform growth 12 of the next 15 years. Growth tends to do best when real interest rates are low, and you could argue interest rates were artificially suppressed from 2010 to 2022. Because more of a growth stock’s value is in the future, the lower the interest rate, the richer their valuation. Rates rose in 2022, temporarily pausing their streak, just in time for AI euphoria to ride to the rescue. Historically, growth stocks become victims of their own success as they gobble up market share and eventually run out of runway. Today, their addressable markets are so large (cloud computing, digital commerce, advertising and AI) that size has been a benefit instead of an anchor. Nvidia, the world’s largest company, just grew revenue 73%. It’s uncommon for the largest company to also be the fastest growing.

Lastly, in the past 10 years only one investment decision really mattered; how much Magnificent Seven did you own? Consisting of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla, if the answer was some, you probably did fine. If not, your money must be under a mattress.

I’ve yet to find a historical precedent for the magnitude of their outperformance. In 2016, if you put $1 in an equal weighted basket of the Mag 7, it’s worth $24 today vs just $3 in the S&P 500. Ten years ago, they were 12% of the benchmark, peaked last year at 33% and created significant concentration risk along the way. The point of an index is diversification, yet in the past five years, the Mag 7 delivered roughly half of the S&P’s return. Somedays, it feels like their economy, we just work here.

I know those are a lot of pictures to process, but I include them to make a point. Markets are supposed to constantly evolve, trends can’t go on forever and nobody wins all the time. Yet large has consistently beaten small, growth has similarly outperformed value, and the Magnificent Seven have trounced just about everything else.

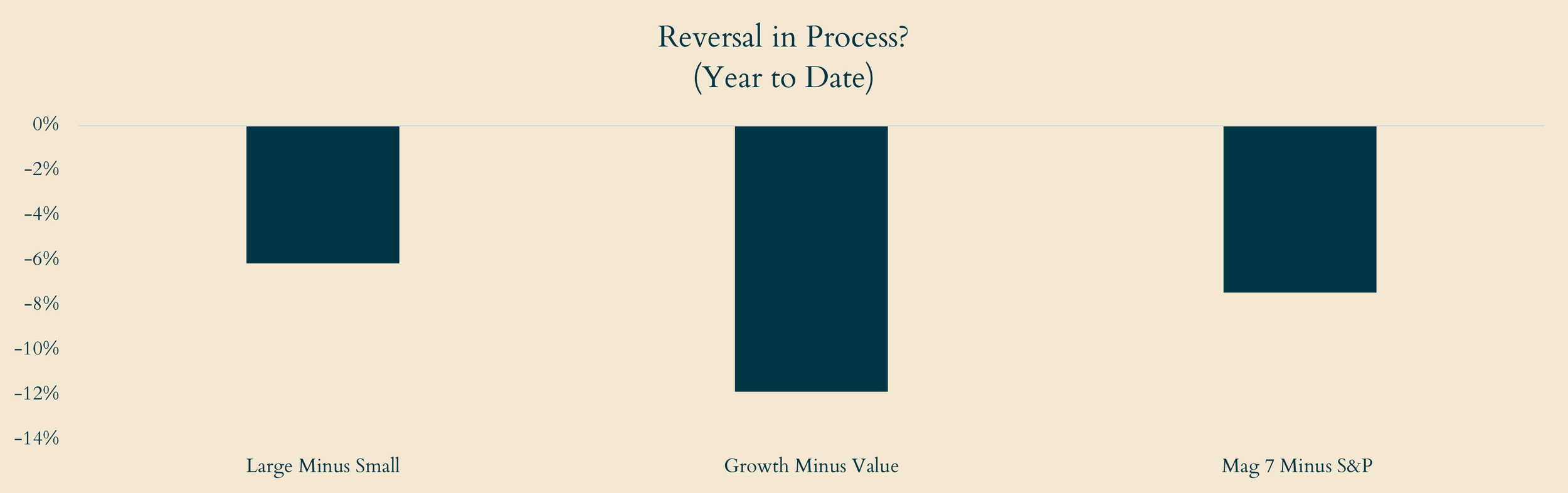

As a small cap manager with a value streak, I’ve avoided making these arguments in the past. Obviously, I’m biased and you’ve heard other contrarians cry wolf long enough. Nor am I suggesting that you shouldn’t own large cap growth or the Magnificent Seven. These are the best companies the world has ever produced and have generated more shareholder value than the other 493 combined. The case I’ve tried to make is that concentration risk is rising and diversification may not always be a drag on performance. It’s worth noting that each of these unstoppable tailwinds recently stopped blowing all at the same time.

I won’t walk you through the reasons for each other than to say that markets are skeptical that astronomical AI capex is being entirely well-spent. They’ve also realized that no one spends such gargantuan sums without plans to take someone else’s market share, causing fear of AI disruption to ripple through several industries, (software being the most notable example). Technological change often causes upheaval, and investors have begun to seek refuge in the kind of old-economy, boring businesses that I specialize in. It’s hard to imagine AI disrupting building products, grocery stores or hospice providers.

No trend would be complete without a memorable acronym and someone recently dubbed the trade HALO (for Heavy Assets, Low Obsolescence). Last month, I mentioned that small caps beat the S&P 500 fourteen days in a row, their longest streak since 1996. There have been false starts in the past, and I won’t hazard a guess if this trend will persist. But markets are starting to appreciate diversification across industry, valuation and cap size, all of which have received short shrift for the past decade.

Regarding the fund, fundraising continues to go well and I remain appreciative that so many of you have given me a fair hearing. Partners just received their K-1s with minimal tax consequences, as I pride myself on the fund’s tax efficiency. The first audit is underway giving me a newfound appreciation for the accounting profession. I’ll continue to report quarterly performance and the fund’s top ten positions one month in arrears. Thank you for your interest in Epigram Capital.

Sincerely,

Dan Walker